The Income Tax Act, 2025 has replaced the Income-tax Act, 1961 with effect from 1 April 2026, introducing a modern and simplified framework for income tax administration in India. One of the most important chapters for taxpayers is the taxation of salary income, as a large number of individuals derive their income from employment.

Although the new law introduces a reorganised structure and simplified drafting style, the basic principles governing taxation of salary remain largely unchanged. The provisions relating to salary, allowances, perquisites and deductions have been arranged more logically to make them easier to understand and apply.

In this article, we explain the salary provisions under the Income Tax Act, 2025, compare them with the corresponding provisions of the Income-tax Act, 1961, and discuss whether there has been any substantive change or merely a renumbering of sections.

Why Should Salaried Employees Understand the New Income Tax Act?

Every salaried employee receives a salary package that may include basic pay, dearness allowance, house rent allowance, bonuses, leave encashment, retirement benefits, perquisites and other allowances. Employers are responsible for deducting Tax Deducted at Source (TDS) from salary before making payment.

With the introduction of the Income Tax Act, 2025, many taxpayers are concerned whether the taxation of salary has changed. The good news is that while the presentation and numbering of provisions have been simplified, the fundamental concepts continue to remain familiar.

Understanding these provisions helps employees correctly compute taxable salary, verify TDS deducted by the employer, claim eligible deductions and file an accurate Income Tax Return.

Salary Provisions Under the Income Tax Act, 2025

The Income Tax Act, 2025 continues to tax salary under the head “Income from Salary.” Salary becomes taxable when it is due from the employer or when it is received, whichever is earlier.

The Act covers all forms of remuneration received by an employee from an employer, including monetary payments as well as taxable benefits and perquisites.

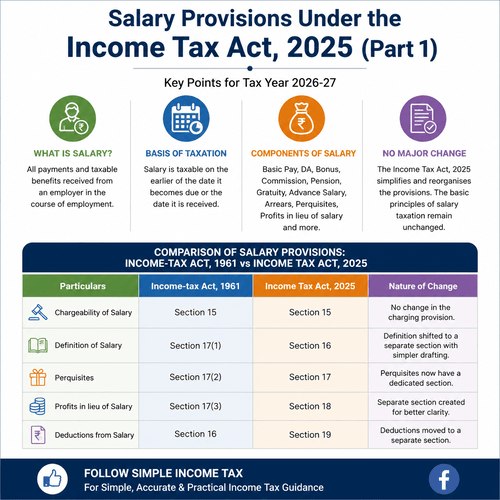

Comparison of Salary Provisions: Income-tax Act, 1961 vs Income Tax Act, 2025

| Particulars | Income-tax Act, 1961 | Income Tax Act, 2025 | Nature of Change |

| Chargeability of Salary | Section 15 | Section 15 | No change in the charging provision. |

| Definition of Salary | Section 17(1) | Section 16 | Definition shifted to a separate section with simpler drafting. |

| Perquisites | Section 17(2) | Section 17 | Perquisites now have a dedicated section. |

| Profits in lieu of Salary | Section 17(3) | Section 18 | Separate section created for better clarity. |

| Deductions from Salary | Section 16 | Section 19 | Deductions moved to a separate section. |

The Income Tax Act, 2025 reorganises the salary provisions into a more logical structure without making major substantive changes in the manner of taxation. Under the Income-tax Act, 1961, the charging provision was contained in Section 15, deductions were provided under Section 16, and the definitions of salary, perquisites and profits in lieu of salary were clubbed together under Section 17.

In contrast, the Income Tax Act, 2025 separates these concepts into independent sections. Section 15 continues to be the charging provision for salary income. The inclusive definition of salary is now contained in Section 16, perquisites are dealt with separately in Section 17, profits in lieu of salary are covered by Section 18, and deductions from salary are provided under Section 19. This restructuring makes the legislation easier to read and navigate while retaining the underlying principles of salary taxation.

Has the Concept of Salary Changed?

The answer is No.

The Income Tax Act, 2025 has not changed the basic concept of salary taxation. Instead, it has reorganised the provisions to improve readability and reduce unnecessary complexity.

Under both the old and the new law, salary includes payments received from an employer in consideration of employment. The objective of the new legislation is simplification rather than changing the taxability of salary.

What Constitutes Salary?

Salary is much more than the monthly amount credited to an employee’s bank account.

It includes various components received from the employer during the course of employment.

Some common components of salary are:

- Basic Pay

- Dearness Allowance (DA)

- Bonus

- Commission

- Fees

- Pension

- Gratuity

- Advance Salary

- Salary Arrears

- Leave Encashment

- Employer’s contribution to specified retirement funds

- Perquisites

- Profits in lieu of salary

Each component may have a different tax treatment depending upon the provisions of the Act.

Basis of Charge of Salary

Salary is taxable on the earlier of:

- When it becomes due, or

- When it is actually received.

This principle has been retained under the Income Tax Act, 2025.

Comparison

| Income-tax Act, 1961 | Income Tax Act, 2025 |

| Salary taxed on due or receipt basis, whichever is earlier | Same principle continues |

Basic Salary

Basic salary forms the foundation of every salary structure. It is fully taxable under both the old and the new Income Tax Acts.

Many other benefits such as Dearness Allowance, House Rent Allowance, gratuity and retirement benefits are linked with the basic salary.

There is no significant change in its tax treatment under the Income Tax Act, 2025.

Dearness Allowance (DA)

Dearness Allowance is paid mainly to Government employees and certain employees in the organised sector to compensate for inflation.

DA forms part of salary and is fully taxable.

Where retirement benefits are calculated after considering DA, it also becomes relevant for computing exemption available for gratuity and other retirement benefits.

Comparison

| Income-tax Act, 1961 | Income Tax Act, 2025 |

| Fully taxable | Fully taxable |

Bonus and Commission

Any bonus or commission received from an employer is taxable as salary.

Whether the bonus is paid monthly, quarterly or annually, it forms part of taxable salary.

Similarly, commission based on sales or turnover also continues to be taxable.

There is no substantive change under the Income Tax Act, 2025.

Advance Salary

Sometimes an employer pays salary before it becomes due.

Such advance salary is taxable in the year of receipt.

However, employees may be eligible for relief where permitted under the law if the advance results in additional tax burden.

The concept remains unchanged under the new Act.

Salary Arrears

Salary arrears arise when an employee receives salary pertaining to an earlier period in a subsequent Tax Year. Under the Income Tax Act, 2025, salary arrears continue to be taxable in the Tax Year in which they are received. In appropriate cases, relief may be available where the receipt of arrears results in a higher tax liability.

Since the taxation of salary arrears, the conditions for claiming relief, the method of computation, and the corresponding provisions under the Income-tax Act, 1961 and the Income Tax Act, 2025 require detailed discussion, these aspects will be covered comprehensively in a separate article in this series, along with practical illustrations and comparative analysis.

This approach keeps the current discussion focused while ensuring that readers receive a complete understanding of the subject in the subsequent article.

Employer-Employee Relationship

Salary can arise only when there is an employer-employee relationship.

Payments received by consultants, freelancers or independent professionals are generally taxed under the head Profits and Gains of Business or Profession, not as salary.

This distinction remains exactly the same under the new Act.

Practical Illustration

Suppose Mr. A receives during the Tax Year:

- Basic Salary – Rs. 9,00,000

- Dearness Allowance – Rs. 1,20,000

- Bonus – Rs. 80,000

His gross salary will be Rs. 11,00,000 before considering deductions and exemptions.

The method of computing salary under the Income Tax Act, 2025 remains substantially similar to the earlier law.

These FAQs are SEO-friendly, written in simple English, and suitable for the end of your article “Salary Provisions Under the Income Tax Act, 2025 (Part 1)”.

Frequently Asked Questions (FAQs)

1. Has the taxation of salary changed under the Income Tax Act, 2025?

No. The basic principles of taxation of salary remain largely unchanged under the Income Tax Act, 2025. The new Act mainly reorganises and simplifies the provisions without making major changes in the manner of taxing salary income.

2. Which section deals with salary under the Income Tax Act, 2025?

Salary continues to be charged to tax under Section 15 of the Income Tax Act, 2025. The charging provision remains the same as under the Income-tax Act, 1961.

3. What is the corresponding section for the definition of salary under the Income Tax Act, 2025?

Under the Income-tax Act, 1961, the definition of salary was contained in Section 17(1). Under the Income Tax Act, 2025, the corresponding provision is Section 16.

4. Has the section relating to perquisites changed under the new Income Tax Act?

Yes. Under the Income-tax Act, 1961, perquisites were covered under Section 17(2). Under the Income Tax Act, 2025, perquisites are dealt with separately under Section 17, making the law easier to understand.

5. Which section deals with deductions from salary under the Income Tax Act, 2025?

Deductions from salary are covered under Section 19 of the Income Tax Act, 2025. Under the Income-tax Act, 1961, these deductions were available under Section 16.

6. Has the due date or basis of taxation of salary changed under the new Act?

No. Salary continues to be taxable on the earlier of the due date or the date of actual receipt. This fundamental principle has been retained under the Income Tax Act, 2025.

7. Will House Rent Allowance (HRA), Leave Travel Allowance (LTA) and other exemptions continue under the Income Tax Act, 2025?

Yes. The Income Tax Act, 2025 continues to provide for various allowances and exemptions, subject to the applicable provisions and rules. The detailed tax treatment of HRA, LTA, perquisites and exemptions will be discussed separately in the subsequent parts of this series.

8. Has the section for TDS on salary changed under the Income Tax Act, 2025?

Yes. Under the Income-tax Act, 1961, TDS on salary was governed by Section 192. Under the Income Tax Act, 2025, the corresponding provision is Section 392. Employers should use the correct provisions while complying with TDS requirements for Tax Year 2026–27 onwards.

9. Will the old section numbers continue to be relevant during Tax Year 2026–27?

During the transition period, many taxpayers, employers and tax professionals may continue referring to the old section numbers. However, it is advisable to gradually adopt the corresponding provisions under the Income Tax Act, 2025 in all tax-related communications and compliance to avoid confusion.

10. What topics will be covered in the next part of this series?

The next part of this series will explain allowances, perquisites, exemptions, valuation rules, retirement benefits, and practical illustrations under the Income Tax Act, 2025. It will also include detailed comparisons with the corresponding provisions of the Income-tax Act, 1961 to help readers understand the changes more easily.

Key Takeaways

The Income Tax Act, 2025 has not fundamentally altered the taxation of salary income. Instead, it simplifies the presentation of the law while retaining the established principles. Salaried employees should therefore focus on understanding the revised structure and section references rather than expecting a complete change in tax treatment.

Access Income Tax Act 2025 here

Related Article : Income Tax Act 2025 Explained