Series: Salary Provisions Under the Income Tax Act 2025 (Part 2)

Introduction

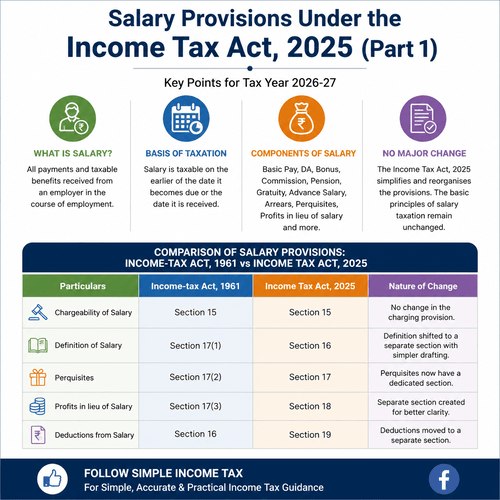

In the first part of this series, we discussed the meaning of salary, basis of charge, salary components and the corresponding provisions under the Income Tax Act 2025.

In this second part, we discuss one of the most important areas of salary taxation—allowances, perquisites and retirement benefits. These components form a significant part of an employee’s salary package and directly affect taxable income as well as the amount of Tax Deducted at Source (TDS) by the employer.

Although the Income Tax Act, 2025 has reorganised the salary provisions into a more structured format, the taxation of allowances and perquisites continues largely on the same principles as under the Income-tax Act, 1961. This article explains these provisions in simple language along with a comparison between the old and the new law.

What are Allowances?

Allowances are fixed monetary payments made by an employer to an employee to meet specific expenses or as additional compensation over and above the basic salary.

Some allowances are fully taxable, while others are wholly or partly exempt subject to prescribed conditions.

Comparison of Allowance Provisions

| Particular | Income-tax Act, 1961 | Income Tax Act, 2025 | Remarks |

| Salary Allowances | Section 10 read with Section 17 | Corresponding exemption provisions retained | No major substantive change |

| HRA Exemption | Section 10(13A) | Corresponding provision under the new Act | Conditions continue |

| Prescribed Rules | Rule 2A | Corresponding Rules | No major change |

The Income Tax Act, 2025 continues the concept of exempt and taxable allowances. However, readers should refer to the corresponding provisions and rules under the new Act while claiming exemptions.

House Rent Allowance (HRA)

House Rent Allowance is one of the most common allowances received by salaried employees residing in rented accommodation.

Employees satisfying the prescribed conditions may claim exemption in respect of HRA. The exemption continues to be calculated based on statutory limits prescribed under the Act and Rules.

Note: A detailed article explaining HRA exemption, calculation, examples and common mistakes will be published separately in this series.

Leave Travel Allowance (LTA)

Leave Travel Allowance is granted to meet travel expenses incurred during leave.

The exemption continues to be available subject to prescribed conditions and limitations.

There is no significant change in the taxability of LTA under the Income Tax Act, 2025.

Dearness Allowance (DA)

Dearness Allowance forms part of salary and is fully taxable.

It also plays an important role in calculating various retirement benefits wherever the terms of employment so provide.

The tax treatment remains unchanged.

Special Allowances

Many employers provide:

- Uniform Allowance

- Children Education Allowance

- Hostel Expenditure Allowance

- Academic Allowance

- Research Allowance

- Daily Allowance

- Conveyance Allowance

Whether these allowances are taxable or exempt depends upon the nature of the allowance and satisfaction of prescribed conditions.

The Income Tax Act, 2025 continues these principles.

What are Perquisites?

Perquisites are benefits or amenities provided by an employer to an employee in addition to salary.

Perquisites may be:

- Taxable

- Partly taxable

- Exempt

The valuation of perquisites is governed by prescribed Rules.

Comparison of Perquisite Provisions

| Income-tax Act, 1961 | Income Tax Act, 2025 |

| Section 17(2) | Section 17 |

| Rules for valuation | Corresponding Rules |

| No major policy change | Simplified drafting |

Unlike the old Act where perquisites formed part of Section 17 itself, the Income Tax Act, 2025 provides a more structured presentation, making the provisions easier to understand.

Common Perquisites

Some common perquisites include:

- Rent-free accommodation

- Concessional accommodation

- Motor car facility

- Free electricity

- Free gas and water

- Interest-free loan

- Domestic servants

- Club membership

- Employer-paid education expenses

- Gifts exceeding prescribed limits

- ESOPs

- Stock options

Each perquisite has its own valuation mechanism.

Employer-Provided Accommodation

Accommodation provided by the employer is one of the most important taxable perquisites.

Its valuation depends upon various factors including:

- Ownership of the accommodation

- Population of the city

- Salary of the employee

- Licence fee recovered

Since the valuation rules are detailed, they will be discussed separately in another article.

Motor Car Facility

Where an employer provides a motor car for official or personal use, the taxable value depends upon:

- Purpose of use

- Engine capacity

- Driver facility

- Employee contribution

Detailed valuation rules remain substantially unchanged.

Interest-Free Loans

Loans provided by employers at concessional rates may constitute taxable perquisites depending upon the amount and applicable interest rates.

However, certain exceptions continue to be available.

ESOPs (Employee Stock Option Plans)

ESOPs remain taxable in accordance with the prescribed provisions.

The point of taxation, valuation methodology and subsequent capital gains implications continue broadly on the same principles.

A separate detailed article will explain ESOP taxation under the Income Tax Act, 2025.

Retirement Benefits

The Income Tax Act, 2025 continues to provide specific provisions regarding retirement benefits such as:

- Gratuity

- Leave Encashment

- Pension

- Commuted Pension

- Uncommuted Pension

- Recognised Provident Fund

- National Pension System (NPS)

The taxation and exemptions relating to these benefits continue largely on the same principles.

Since each benefit has detailed exemption conditions, separate articles will cover them comprehensively.

Comparison of Retirement Benefits

| Benefit | Income-tax Act, 1961 | Income Tax Act, 2025 |

| Gratuity | Exemption available | Continues |

| Leave Encashment | Exemption available | Continues |

| Pension | Taxable subject to exemptions | Continues |

| NPS | Eligible benefits continue | Continues |

Key Changes under the Income Tax Act, 2025

Although the presentation has changed, the following aspects remain substantially unchanged:

- Taxability of allowances

- Perquisite valuation principles

- Retirement benefit taxation

- Employer-provided accommodation

- Motor car valuation

- Interest-free loan taxation

The major change is the simplified legislative structure and improved readability.

Key Takeaways

The Income Tax Act, 2025 does not fundamentally alter the taxation of allowances, perquisites or retirement benefits. Instead, it reorganises the provisions into a more logical framework while preserving the established principles. Salaried employees should continue to maintain proper records for claiming exemptions and accurately report taxable perquisites while filing their Income Tax Return.

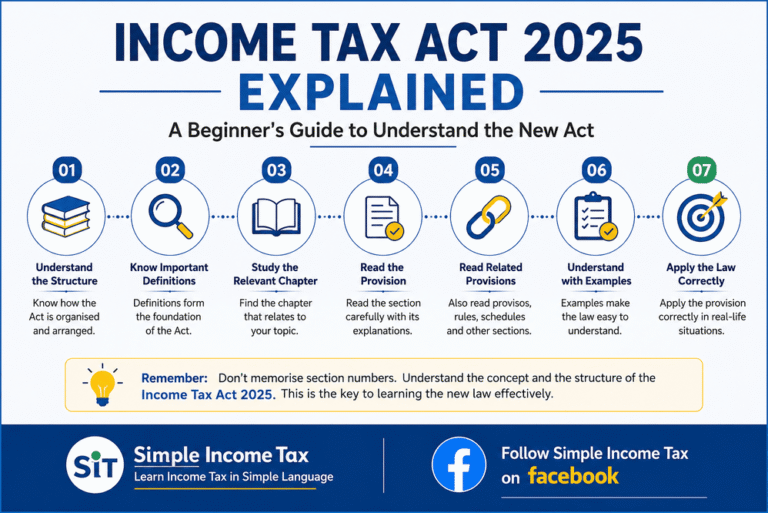

Utility to check provisions of Income-tax Act, 1961 vis-a-vis Income-tax Act, 2025

Related Article

Salary Provisions Under Income Tax Act 2025 – Part 1