Series : Salary Provisions Under the Income Tax Act 2025 (Part 3)

In the first two parts of this series, we discussed the meaning of salary, salary components, allowances, perquisites and retirement benefits under the Income Tax Act, 2025. Understanding these provisions is essential because they form the basis for computing an employee’s taxable salary. In this series, we discuss Salary Deductions, TDS on Salary, Advance Tax & Employer Compliance under the Income Tax Act, 2025

Once the taxable salary has been determined, the next step is to calculate the tax liability, deduct tax at source (TDS), deposit the tax with the Government and comply with various statutory requirements. These responsibilities are primarily discharged by the employer, while employees should verify the correctness of tax deductions and ensure proper reporting while filing their Income Tax Returns.

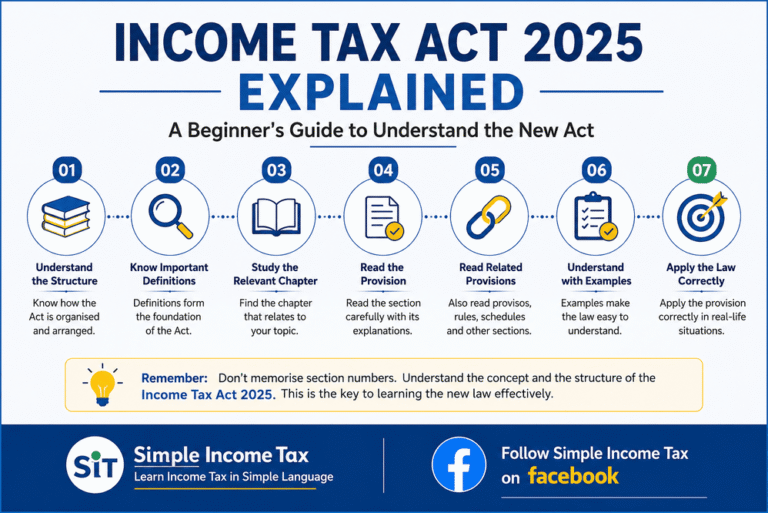

The Income Tax Act 2025 reorganises these compliance provisions into a simpler framework. Although the section numbers have changed, the fundamental principles continue to remain substantially the same.

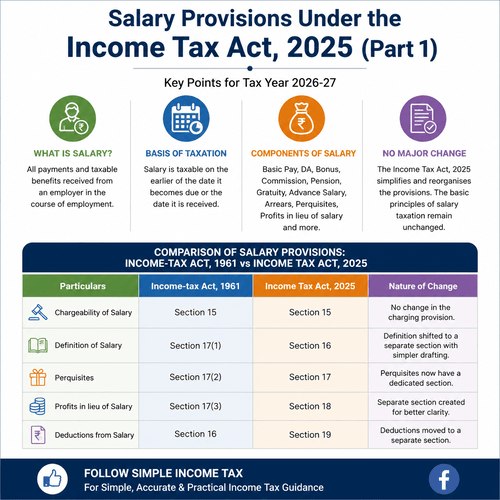

Salary Deductions under the Income Tax Act, 2025

Before calculating the taxable income under the head Income from Salary, certain deductions are allowed from the gross salary.

These deductions reduce the taxable salary and consequently reduce the amount of TDS deductible by the employer.

Comparison of Salary Deductions

| Particulars | Income-tax Act, 1961 | Income Tax Act, 2025 | Remarks |

| Deductions from Salary | Section 16 | Section 19 | Section renumbered and simplified |

| Standard Deduction | Section 16(ia) | Section 19 | Continues |

| Entertainment Allowance | Section 16(ii) | Section 19 | Continues |

| Professional Tax | Section 16(iii) | Section 19 | Continues |

The Income Tax Act, 2025 consolidates all deductions from salary under Section 19, making the law easier to understand.

Standard Deduction

One of the most important deductions available to salaried employees is the Standard Deduction.

This deduction is available without requiring the employee to produce bills or vouchers. Eligible employees can claim the deduction subject to the limits prescribed by law.

Although the section number has changed under the Income Tax Act, 2025, the concept of standard deduction continues.

A separate article will discuss the history, eligibility, amount, recent amendments and practical examples relating to Standard Deduction.

Entertainment Allowance

Entertainment Allowance continues to be available as a deduction in specified cases, particularly for eligible Government employees, subject to statutory conditions.

Since the provisions are technical and applicable only in limited situations, they will be discussed separately in another article.

Professional Tax

Professional Tax paid by an employee continues to qualify for deduction from salary where permissible under the applicable law.

The Income Tax Act, 2025 does not introduce any major substantive change in this regard.

TDS on Salary

Every employer responsible for paying salary is required to deduct Tax Deducted at Source (TDS) before making payment to the employee whenever the estimated taxable income exceeds the basic exemption limit or other applicable threshold.

The employer has to estimate the employee’s annual taxable salary, consider eligible deductions, exemptions and declarations furnished by the employee and thereafter deduct tax throughout the Tax Year.

Comparison of TDS on Salary

| Particulars | Income-tax Act, 1961 | Income Tax Act, 2025 | Remarks |

| TDS on Salary | Section 192 | Section 392 | Renumbered |

| TDS Certificate | Form 16 | Form 16 | Continues |

| Salary Statement | Form 24Q | Form 24Q (subject to future modifications) | Continues during transition |

One of the significant structural changes under the Income Tax Act, 2025 is that Section 392 now governs deduction of tax from salary. Although the section number has changed from Section 192 to Section 392, the underlying principles remain substantially unchanged.

Employer’s Responsibilities

Every employer should:

- Estimate annual salary.

- Obtain employee declarations.

- Consider eligible deductions.

- Deduct TDS correctly.

- Deposit TDS within prescribed time.

- File quarterly TDS statements.

- Issue Form 16.

- Correct mistakes through revised statements where necessary.

Failure to comply may result in interest, penalty or other consequences under the Income Tax Act.

Employee’s Responsibilities

Employees should:

- Submit investment declarations.

- Intimate previous employer’s salary.

- Choose the applicable tax regime.

- Verify Form 16.

- Check Form 26AS, AIS and TIS.

- Report all salary income correctly while filing the Income Tax Return.

Advance Tax

Many salaried employees assume that they never have to pay Advance Tax.

This is not always correct.

Where TDS deducted by the employer is insufficient or where the employee has substantial income from other sources, Advance Tax may become payable.

Comparison of Advance Tax Provisions

| Particulars | Income-tax Act, 1961 | Income Tax Act, 2025 |

| Liability to pay Advance Tax | Section 207 | Section 403 |

| Conditions | Section 208 | Section 404 |

| Computation | Section 209 | Section 405 |

| Payment by Assessee | Section 210 | Section 406 |

| Payment pursuant to AO’s order | Section 210 | Section 407 |

| Instalments | Section 211 | Section 408 |

Although the provisions have been renumbered, the concept of Advance Tax remains substantially unchanged.

A separate article will explain Advance Tax, due dates, computation, interest and practical illustrations.

Self-Assessment Tax (SAT)

Where any tax remains payable after considering TDS, Advance Tax and reliefs, the balance tax has to be paid before filing the Income Tax Return.

Comparison of Self-Assessment Tax

| Income-tax Act, 1961 | Income Tax Act, 2025 |

| Section 140A | Section 413 |

The procedure, computation and practical issues relating to Self-Assessment Tax will be discussed separately in another article.

Interest for Default

Failure to pay Advance Tax or delay in payment may attract statutory interest.

| Income-tax Act, 1961 | Income Tax Act, 2025 |

| Section 234B | Section 424 |

| Section 234C | Section 425 |

Detailed discussion on these provisions will be covered separately.

Important Transition for Tax Year 2026–27

Since Tax Year 2026–27 is the first year under the Income Tax Act, 2025, taxpayers, employers, DDOs and tax professionals may continue to refer to the old section numbers.

For example:

| Old Section | New Section |

| Section 192 | Section 392 |

| Section 207 | Section 403 |

| Section 208 | Section 404 |

| Section 209 | Section 405 |

| Section 210 | Section 406 & 407 |

| Section 211 | Section 408 |

| Section 140A | Section 413 |

| Section 234B | Section 424 |

| Section 234C | Section 425 |

It is advisable to gradually adopt the new section references in professional practice and official correspondence.

Here are 10 SEO-friendly FAQs for Part 3: Salary Deductions, TDS on Salary, Advance Tax & Employer Compliance under the Income Tax Act, 2025. These FAQs are written in simple English and include practical questions that readers are likely to search for.

Frequently Asked Questions (FAQs)

1. Which section governs TDS on salary under the Income Tax Act, 2025?

Under the Income Tax Act, 2025, Section 392 governs the deduction of tax at source (TDS) from salary. It corresponds to Section 192 of the Income-tax Act, 1961. Although the section number has changed, the basic principles for deducting TDS from salary remain substantially the same.

2. Is TDS deducted every month from salary?

Yes. Employers generally deduct TDS every month based on the estimated annual taxable salary of the employee. The tax liability is spread over the remaining months of the Tax Year to ensure proper compliance.

3. What documents should an employee submit to the employer for correct TDS deduction?

Employees should submit investment declarations, proof of eligible deductions and exemptions, details of previous employment, income from house property (where applicable), and any other information required by the employer for accurate computation of taxable salary and TDS.

4. Which section provides deductions from salary under the Income Tax Act, 2025?

Deductions from salary are provided under Section 19 of the Income Tax Act, 2025. This section corresponds to Section 16 of the Income-tax Act, 1961 and includes deductions such as the Standard Deduction, Entertainment Allowance (in eligible cases), and Professional Tax.

5. Is Advance Tax applicable to salaried employees?

Yes. Although TDS usually covers the tax liability of salaried employees, Advance Tax may become payable if the employee has additional income, such as interest, rental income, capital gains or business income, and the total tax liability remaining after TDS exceeds the prescribed limit.

6. Which sections deal with Advance Tax under the Income Tax Act, 2025?

The Advance Tax provisions are contained in Sections 403 to 408 of the Income Tax Act, 2025, corresponding to Sections 207 to 211 of the Income-tax Act, 1961.

7. What is Self-Assessment Tax under the Income Tax Act, 2025?

Self-Assessment Tax is the balance tax payable by the taxpayer after adjusting TDS, Advance Tax, reliefs and tax credits. Under the Income Tax Act, 2025, the relevant provision is Section 413, which corresponds to Section 140A of the Income-tax Act, 1961.

8. What happens if the employer deducts less TDS from salary?

If insufficient TDS is deducted, the employee remains responsible for paying the balance tax. Depending on the circumstances, the employee may also be liable to pay interest for short payment of Advance Tax or Self-Assessment Tax under the applicable provisions of the Income Tax Act.

9. Should employers and taxpayers use the new section numbers during Tax Year 2026–27?

Yes. Since Tax Year 2026–27 is the first year of implementation of the Income Tax Act, 2025, employers, Drawing and Disbursing Officers (DDOs), tax professionals and taxpayers should gradually adopt the new section numbers in tax computations, correspondence and compliance documents to avoid confusion during the transition.

10. What topics will be covered in Part 4 of this series?

The next part of this series will cover practical salary computation examples, TDS calculation, common mistakes made by salaried taxpayers, old versus new section mapping, employer compliance checklist, and frequently encountered issues while filing the Income Tax Return under the Income Tax Act, 2025.

Key Takeaways

The Income Tax Act, 2025 simplifies the structure of salary-related compliance provisions without substantially changing the legal principles. Employers should familiarise themselves with the new section numbers governing TDS, salary deductions and advance tax, while employees should verify tax deductions, maintain supporting documents and ensure accurate reporting in their Income Tax Returns.

Related Article

Salary Provisions Under Income Tax Act 2025 – Part 1

Salary Allowances & Perquisites Under Income Tax Act 2025