Series: Salary Provisions Under the Income Tax Act, 2025 (Part 4)

In the previous three parts of this series, we discussed the provisions relating to salary income, allowances, perquisites, retirement benefits, salary deductions, Tax Deducted at Source (TDS), Advance Tax and employer compliance under the Income Tax Act, 2025.

In this concluding part, we bring together all these concepts through practical illustrations, explain the common mistakes committed by salaried taxpayers and employers, and provide answers to frequently asked questions. Understanding these practical aspects will help taxpayers correctly compute their taxable salary, verify the TDS deducted by the employer and file an accurate Income Tax Return.

Steps for Computing Taxable Salary

The computation of taxable salary should generally follow the following sequence:

- Compute Gross Salary.

- Add taxable allowances.

- Add taxable perquisites.

- Add profits in lieu of salary, if any.

- Deduct eligible deductions under Section 19 of the Income Tax Act, 2025.

- Arrive at Income under the head “Income from Salary”.

- Add income from other heads, if applicable.

- Compute total tax liability.

- Reduce TDS deducted under Section 392, Advance Tax and other tax credits.

- Pay Self-Assessment Tax under Section 413, if any balance tax remains.

Practical Illustration – 1

Basic Salary Case

Mr. A receives during Tax Year 2026–27:

- Basic Salary – Rs. 8,40,000

- Dearness Allowance – Rs. 1,20,000

- Bonus – Rs. 60,000

- Standard Deduction – As admissible under the Act

After considering the admissible deduction, the balance shall be taxable under the head Income from Salary.

The employer shall estimate the tax liability and deduct TDS under Section 392.

Practical Illustration – 2

Salary with HRA

Mrs. B receives:

- Basic Salary

- Dearness Allowance

- House Rent Allowance

- Bonus

She resides in rented accommodation and satisfies the prescribed conditions for claiming HRA exemption.

The exempt portion of HRA shall be excluded from taxable salary while computing TDS.

The detailed method of computing HRA exemption has been discussed separately in the article dedicated to HRA under the Income Tax Act, 2025.

Practical Illustration – 3

Salary with Perquisites

Mr. C receives:

- Basic Salary

- Motor Car Facility

- Rent-free Accommodation

- Employer-paid Medical Insurance

The taxable value of each perquisite shall be determined in accordance with the prescribed rules and added to salary before computing tax liability.

Practical Illustration – 4

Additional Income

An employee receives salary and also earns:

- Bank Interest

- Rental Income

Although the employer deducts TDS on salary, the employee may still become liable to pay Advance Tax under Sections 403 to 408 of the Income Tax Act, 2025 if the tax payable after TDS exceeds the prescribed limit.

Common Mistakes Made by Salaried Employees

Many salaried taxpayers make avoidable mistakes while computing income or filing their Income Tax Returns. Some of the common errors are:

- Not verifying Form 16 before filing the return.

- Ignoring salary received from a previous employer.

- Claiming ineligible exemptions or deductions.

- Not reporting interest income or rental income.

- Failing to include taxable perquisites.

- Choosing the wrong tax regime without proper comparison.

- Assuming that TDS deducted by the employer is always correct.

- Ignoring Form 26AS, AIS and TIS before filing the return.

- Not paying Self-Assessment Tax where balance tax is payable.

- Using old section numbers under the repealed Income-tax Act, 1961 in professional correspondence during the transition period.

Common Mistakes Made by Employers

Employers should also avoid certain compliance errors, such as:

- Incorrect estimation of annual taxable salary.

- Failure to consider declarations submitted by employees.

- Delayed deduction or deposit of TDS.

- Incorrect reporting in quarterly TDS statements.

- Delay in issuing Form 16.

- Failure to revise incorrect TDS returns.

- Quoting incorrect section numbers while referring to the Income Tax Act, 2025.

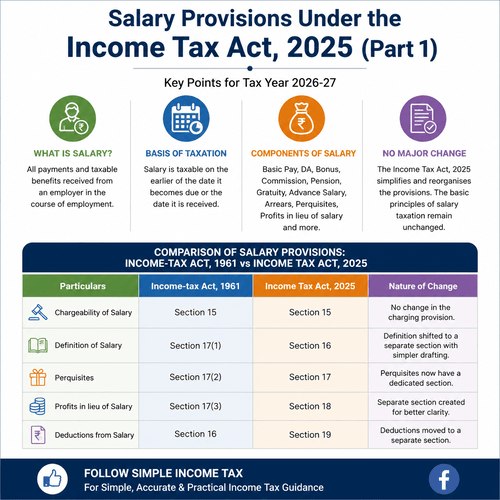

Old vs New Section Mapping

| Income-tax Act, 1961 | Income Tax Act, 2025 |

| Section 15 | Section 15 |

| Section 16 | Section 19 |

| Section 17(1) | Section 16 |

| Section 17(2) | Section 17 |

| Section 17(3) | Section 18 |

| Section 192 | Section 392 |

| Section 207 | Section 403 |

| Section 208 | Section 404 |

| Section 209 | Section 405 |

| Section 210 | Sections 406 & 407 |

| Section 211 | Section 408 |

| Section 140A | Section 413 |

| Section 234B | Section 424 |

| Section 234C | Section 425 |

Salary Compliance Checklist for Employees

Before filing the Income Tax Return, every salaried employee should ensure that:

- Salary income has been correctly reported.

- Form 16 has been verified.

- Form 26AS has been checked.

- Annual Information Statement (AIS) has been reviewed.

- Tax Information Statement (TIS) has been verified.

- Eligible deductions have been claimed.

- Tax regime has been selected carefully.

- Self-Assessment Tax has been paid, if required.

- Bank account details have been verified.

- Return has been e-Verified after filing.

Practical Examples under the Income Tax Act, 2025

Example 1: Basic Salary Only

Situation

Mr. A is employed in a private company and receives only Basic Salary of Rs. 8,40,000 during the Tax Year 2026–27. He does not receive any allowances or perquisites.

Tax Treatment

The Basic Salary forms part of taxable salary under Section 15 of the Income Tax Act, 2025. Mr. A will be eligible for deductions under Section 19, wherever applicable.

Example 2: Basic Salary with Dearness Allowance

Situation

Mrs. B receives:

- Basic Salary – Rs. 9,00,000

- Dearness Allowance – Rs. 1,50,000

Tax Treatment

Dearness Allowance forms part of salary and is fully taxable. It is also considered for certain retirement benefits wherever the terms of employment so provide.

Example 3: Salary with House Rent Allowance (HRA)

Situation

Mr. C resides in rented accommodation and receives HRA from his employer.

Tax Treatment

HRA exemption shall be computed according to the prescribed provisions under the Income Tax Act and Rules. Only the exempt portion will be excluded from taxable salary, while the balance HRA will remain taxable.

Example 4: Salary with Leave Travel Allowance (LTA)

Situation

Mrs. D claims Leave Travel Allowance while travelling with her family during leave.

Tax Treatment

LTA exemption is available only if the prescribed conditions are fulfilled. Expenses not qualifying under the rules shall remain taxable.

Example 5: Salary with Bonus

Situation

Mr. E receives an annual performance bonus of Rs. 1,20,000.

Tax Treatment

Bonus received from the employer forms part of salary income and is fully taxable in the Tax Year in which it is received or becomes due, whichever is earlier.

Example 6: Salary with Commission

Situation

A sales executive receives Basic Salary and commission based on annual sales.

Tax Treatment

Commission received from the employer is taxable as salary and shall be included while computing taxable income.

Example 7: Salary with Rent-Free Accommodation

Situation

An employer provides furnished accommodation to an employee.

Tax Treatment

The value of rent-free accommodation shall be determined as per the prescribed valuation rules and added to taxable salary as a perquisite.

Example 8: Salary with Motor Car Facility

Situation

An employee is provided a motor car by the employer for both official and personal purposes.

Tax Treatment

The taxable value of the motor car perquisite shall be determined in accordance with the prescribed valuation rules after considering official and personal use.

Example 9: Salary with Interest-Free Loan

Situation

An employer grants an interest-free housing loan to an employee.

Tax Treatment

The concessional benefit may be treated as a taxable perquisite unless covered by any prescribed exemption.

Example 10: Salary with Employer’s Contribution to NPS

Situation

The employer contributes to the employee’s National Pension System (NPS) account.

Tax Treatment

The taxability and deduction shall be governed by the applicable provisions relating to employer contribution to NPS under the Income Tax Act, 2025.

Example 11: Salary with Gratuity

Situation

An employee retires after completing long service and receives gratuity.

Tax Treatment

Gratuity shall be taxable or exempt depending upon the category of employee and the applicable exemption provisions.

Example 12: Salary with Leave Encashment

Situation

An employee receives leave encashment at the time of retirement.

Tax Treatment

The exemption shall be available subject to the prescribed conditions and limits under the Income Tax Act.

Example 13: Salary Arrears

Situation

An employee receives salary arrears relating to earlier years.

Tax Treatment

Salary arrears are taxable in the year of receipt. Relief, if admissible, may be claimed in accordance with the applicable provisions.

Example 14: Advance Salary

Situation

An employer pays six months’ salary in advance.

Tax Treatment

Advance Salary is taxable in the year of receipt. Relief may be available where permitted under the Act.

Example 15: Salary from Two Employers

Situation

An employee changes jobs during the Tax Year and receives salary from two employers.

Tax Treatment

Salary received from both employers is taxable. The employee should furnish details of the previous employer to the new employer for correct deduction of TDS under Section 392.

Example 16: Salary with Bank Interest

Situation

An employee earns salary and also receives bank interest.

Tax Treatment

While TDS may have been correctly deducted on salary, the employee must also include interest income while filing the Income Tax Return. Additional tax liability may arise.

Example 17: Salary with Rental Income

Situation

An employee owns a residential house which has been let out.

Tax Treatment

Rental income is taxable under the appropriate head of income and should be included while computing the total tax liability.

Example 18: Salary with Capital Gains

Situation

An employee sells listed shares during the Tax Year.

Tax Treatment

Capital gains are taxable separately and should be disclosed while filing the Income Tax Return.

Example 19: Liability to Pay Advance Tax

Situation

A salaried employee receives substantial interest income and capital gains.

Tax Treatment

If the tax liability remaining after TDS exceeds the prescribed threshold, the employee may be required to pay Advance Tax under Sections 403 to 408 of the Income Tax Act, 2025.

Example 20: Payment of Self-Assessment Tax

Situation

After considering TDS and Advance Tax, an employee still has a balance tax liability while filing the Income Tax Return.

Tax Treatment

The balance tax should be paid as Self-Assessment Tax under Section 413 before filing the return.

Example 21: Incorrect TDS Deduction by Employer

Situation

The employer inadvertently deducts less TDS than required.

Tax Treatment

The employee remains liable to pay the correct tax. Depending on the circumstances, interest may also become payable under the relevant provisions.

Example 22: Failure to Submit Investment Proofs

Situation

An employee does not submit the required investment proofs to the employer within the stipulated time.

Tax Treatment

The employer may compute TDS without considering the claimed deductions or exemptions. The employee can claim eligible benefits while filing the Income Tax Return, subject to satisfying the legal requirements.

Example 23: Incorrect Tax Regime Selection

Situation

An employee opts for a tax regime without comparing the available benefits.

Tax Treatment

Selecting an unsuitable regime may increase the tax liability. Taxpayers should evaluate both options before exercising the choice available under the law.

Example 24: Mismatch Between Form 16 and Return

Situation

The salary reported in the Income Tax Return does not match the details in Form 16.

Tax Treatment

Such mismatches may result in processing delays, notices or the need for clarification. Employees should reconcile Form 16, Form 26AS, AIS and TIS before filing the return.

Example 25: Comprehensive Salary Computation

Situation

An employee receives Basic Salary, Dearness Allowance, HRA, Bonus, employer-provided accommodation, employer’s contribution to NPS and bank interest.

Tax Treatment

The employee should:

- Compute Gross Salary under Section 15.

- Add taxable allowances and perquisites.

- Claim eligible deductions under Section 19.

- Include income from other heads.

- Compute total tax liability.

- Reduce TDS deducted under Section 392.

- Adjust Advance Tax paid under Sections 403–408.

- Pay any remaining Self-Assessment Tax under Section 413 before filing the Income Tax Return.

Frequently Asked Questions (FAQs)

1. How is taxable salary computed under the Income Tax Act, 2025?

Taxable salary is computed by adding all taxable salary components, allowances, perquisites and profits in lieu of salary, and then reducing the deductions available under Section 19 of the Income Tax Act, 2025. The resulting amount is taxable under the head Income from Salary.

2. Which section charges salary to tax under the Income Tax Act, 2025?

Salary is chargeable to tax under Section 15 of the Income Tax Act, 2025. The basic principle of taxation remains the same as under the Income-tax Act, 1961.

3. Which section governs TDS on salary under the Income Tax Act, 2025?

TDS on salary is governed by Section 392 of the Income Tax Act, 2025, corresponding to Section 192 of the Income-tax Act, 1961.

4. Is Form 16 still relevant under the Income Tax Act, 2025?

Yes. Form 16 continues to be an important document issued by the employer showing salary paid and TDS deducted. Employees should verify the details before filing their Income Tax Return.

5. Should I rely only on Form 16 while filing my Income Tax Return?

No. Apart from Form 16, you should also verify Form 26AS, Annual Information Statement (AIS) and Taxpayer Information Statement (TIS) to ensure that all income and taxes are correctly reflected.

6. What happens if my employer deducts less TDS?

If insufficient TDS has been deducted by the employer, the employee remains liable to pay the correct tax. Interest may also become payable depending on the circumstances.

7. Can a salaried employee be required to pay Advance Tax?

Yes. If a salaried employee has additional income such as interest, rental income or capital gains, and the tax payable after adjusting TDS exceeds the prescribed limit, Advance Tax may be payable.

8. Which sections deal with Advance Tax under the Income Tax Act, 2025?

Advance Tax is governed by Sections 403 to 408 of the Income Tax Act, 2025.

9. What is Self-Assessment Tax?

Self-Assessment Tax is the balance tax payable by the taxpayer after adjusting TDS, Advance Tax and other eligible tax credits. It is governed by Section 413 of the Income Tax Act, 2025.

10. Is salary from my previous employer taxable?

Yes. Salary received from both the previous and current employer during the same Tax Year is taxable. Employees should disclose the salary received from the previous employer to ensure correct TDS deduction.

11. Are salary arrears taxable?

Yes. Salary arrears are generally taxable in the year of receipt. Relief may be available in eligible cases as per the applicable provisions of the Income Tax Act.

12. Is advance salary taxable?

Yes. Advance salary is generally taxable in the year of receipt, even if it relates to a future period. Relief may be available in specified circumstances.

13. What are the common mistakes made by salaried taxpayers while filing their Income Tax Return?

Common mistakes include:

- Not reporting salary from a previous employer.

- Ignoring interest income.

- Claiming incorrect deductions.

- Not verifying Form 16 and Form 26AS.

- Choosing the wrong tax regime.

- Not paying Self-Assessment Tax before filing the return.

14. Should I check AIS before filing my return?

Yes. AIS contains information relating to salary, interest, securities transactions and other financial transactions. It helps taxpayers reconcile their income before filing the return.

15. What is the difference between AIS and Form 26AS?

Form 26AS mainly contains information relating to TDS, TCS and specified tax payments, whereas AIS provides a much wider range of financial information, including salary, interest, securities transactions and other reported transactions.

16. Which documents should every salaried employee keep before filing the Income Tax Return?

Employees should keep:

- Form 16

- Form 26AS

- AIS

- TIS

- Salary slips

- Investment proofs

- Bank interest certificates

- Home loan interest certificate, if applicable

- Rent receipts, where applicable

17. Can I claim deductions if I did not submit investment proofs to my employer?

Yes. If you are otherwise eligible under the Income Tax Act, you may claim the deductions while filing your Income Tax Return, subject to the applicable provisions and supporting evidence.

18. Why is it important to use the new section numbers under the Income Tax Act, 2025?

Since Tax Year 2026–27 is the first year under the new Act, using the correct section numbers helps avoid confusion and ensures consistency in professional correspondence and tax compliance.

19. What should employers do to ensure correct TDS deduction?

Employers should obtain employee declarations, estimate annual taxable salary correctly, consider eligible deductions and exemptions, deduct TDS under Section 392, deposit the tax on time and issue Form 16 after filing the prescribed TDS statements.

20. Where can I find the complete guide to salary taxation under the Income Tax Act, 2025?

This article is the concluding part of the “Salary Provisions Under the Income Tax Act, 2025” series. Readers may also refer to:

- Part 1: Salary Income, Basis of Charge & Salary Components

- Part 2: Allowances, Perquisites & Retirement Benefits

- Part 3: Salary Deductions, TDS, Advance Tax & Employer Compliance

Together, these four parts provide a comprehensive guide to salary taxation under the Income Tax Act, 2025 for Tax Year 2026–27.

Key Takeaways

The Income Tax Act, 2025 has modernised the legislative framework for taxation of salary without significantly changing the underlying principles. Salaried taxpayers should familiarise themselves with the new section numbers, verify TDS deductions, maintain proper documentation and ensure timely compliance.

Employers should update their payroll systems, TDS manuals and internal procedures to align with the provisions of the new Act. Correct compliance during the transition period will help minimise disputes and facilitate smooth processing of Income Tax Returns.

Conclusion

The Income Tax Act, 2025 marks an important milestone in India’s direct tax law by presenting salary provisions in a simpler and more structured manner. While the concepts of salary, allowances, perquisites, deductions and TDS remain broadly similar to those under the Income-tax Act, 1961, taxpayers and employers must become familiar with the revised statutory framework and corresponding section numbers.

This four-part series has explained the key salary provisions applicable for Tax Year 2026–27, compared them with the earlier law and highlighted practical issues that may arise during the transition. Readers are encouraged to refer to the official notifications, rules and circulars issued by the CBDT from time to time, as procedural requirements and compliance formats may continue to evolve during the implementation of the new Act.

Related Article in this series

- Income Tax Act 2025 Explained

- Salary Provisions Under Income Tax Act 2025 – Part 1

- Salary Allowances & Perquisites Under Income Tax Act 2025

- Salary TDS & Deductions Under Income Tax Act 2025

Disclaimer: These articles are intended for educational and general informational purposes only. While every effort has been made to ensure accuracy, readers are advised to verify the latest provisions, notifications, circulars, rules and forms on the official Income Tax Department website before taking any tax-related decision. In case of any inconsistency, the provisions of the applicable law and official notifications shall prevail.