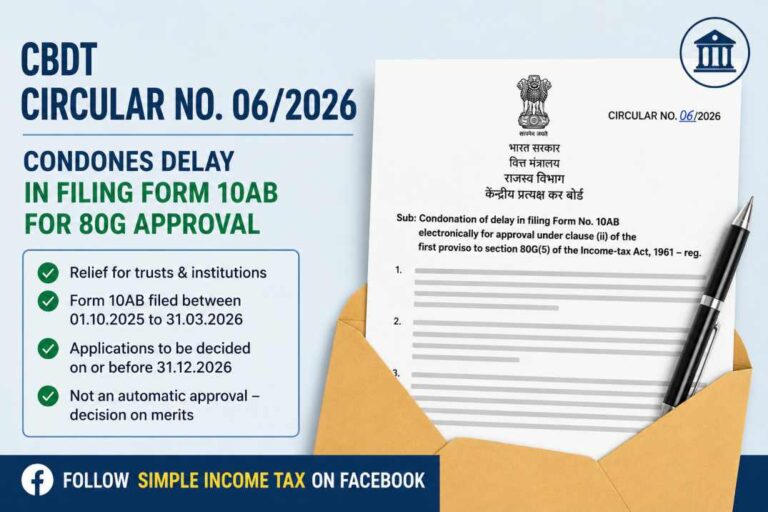

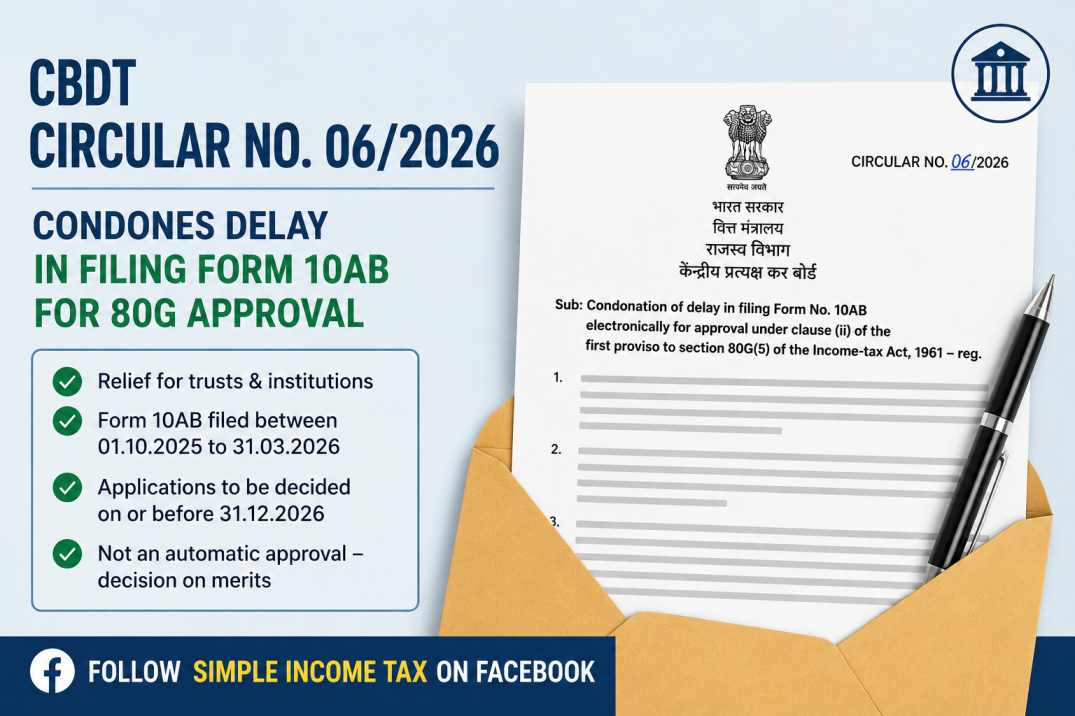

The Central Board of Direct Taxes (CBDT) has issued Circular No. 06/2026, providing significant relief to charitable trusts, institutions and funds that could not file Form No. 10AB within the prescribed due date for renewal of approval under Section 80G(5) of the Income Tax Act. The circular condones delay in filing Form 10AB in eligible cases and allows such applications to be considered on merits. This decision is expected to benefit many charitable organisations that were unable to comply with the statutory timeline due to genuine reasons.

What is Form No. 10AB?

Section 80G of the Income Tax Act allows taxpayers to claim deduction for donations made to approved charitable funds and institutions. However, trusts and institutions enjoying approval under Section 80G are required to renew their approval before its expiry.

For this purpose, they must electronically file Form No. 10AB at least six months before the expiry of the approval period. Failure to file the application within the prescribed time may result in difficulties in obtaining continued approval.

Why Was This Circular Issued?

The CBDT received several representations from charitable trusts and institutions whose 80G approval was due to expire on 31 March 2026. Many of these organisations could not submit Form No. 10AB before the prescribed due date of 30 September 2025.

According to the representations received by the Board, the delay occurred due to bona fide reasons and circumstances beyond their control, causing genuine hardship to organisations that depend upon donations for carrying out charitable activities. Considering these difficulties, the CBDT examined the matter and decided to grant relief through this circular.

CBDT Condones Delay in Filing Form 10AB

Exercising its powers under Section 119(2)(b) of the Income Tax Act, 1961, read with Section 536(2) of the Income Tax Act, 2025, the CBDT has condoned the delay in filing Form No. 10AB in specified cases.

The relief applies where Form No. 10AB has been filed electronically between 1 October 2025 and 31 March 2026. Such delayed applications will now be considered valid, and the jurisdictional Principal Commissioner of Income Tax or Commissioner of Income Tax has been authorised to examine these applications on merits and pass suitable orders.

What Happens to Applications Already Rejected?

The circular also provides relief to institutions whose applications were already rejected solely because Form No. 10AB was filed after the prescribed due date.

If an application filed electronically between 1 October 2025 and 31 March 2026 was rejected only on the ground of delay, such delay shall now be treated as condoned. The concerned Principal Commissioner of Income Tax or Commissioner of Income Tax will reconsider these applications on merits and pass appropriate orders. This ensures that genuine applicants are not denied approval merely because of delayed filing.

Time Limit for Disposal of Applications

The CBDT has directed that all eligible applications covered by this circular should be disposed of by the jurisdictional authorities on or before 31 December 2026.

This provides certainty to charitable organisations regarding the timeline within which their applications are expected to be decided.

Important Points to Remember

The circular provides important relief, but it does not grant automatic approval.

Every application will still be examined by the jurisdictional Principal Commissioner or Commissioner of Income Tax. Approval will be granted only after considering the merits of each case and verifying whether all statutory conditions are fulfilled.

Therefore, charitable institutions should ensure that all supporting documents and required information are complete while pursuing their applications.

Who Will Benefit from This Circular?

The circular is expected to benefit:

- Charitable trusts

- Religious institutions eligible under Section 80G

- Educational institutions

- Medical institutions

- Funds and societies seeking renewal of 80G approval

Many organisations that faced genuine difficulties in meeting the original filing deadline now have an opportunity to have their applications considered without suffering adverse consequences merely due to delay.

Why This Circular is Important

Approval under Section 80G is extremely important for charitable institutions because it enables donors to claim deduction for donations made to such organisations.

If approval expires due to procedural delays, donors may lose tax benefits, which can adversely affect fundraising activities. By condoning the delay in filing Form No. 10AB, the CBDT has removed a major procedural hurdle and provided relief to genuine charitable institutions.

The circular also reflects the Board’s approach of addressing genuine hardship where procedural non-compliance occurred for bona fide reasons while maintaining scrutiny of applications on merits.

Final Thoughts

CBDT Circular No. 06/2026 is a welcome relief for charitable trusts and institutions that could not file Form No. 10AB within the prescribed time. Instead of rejecting applications merely on technical grounds, the Board has allowed delayed applications to be considered on merits, thereby balancing procedural compliance with genuine hardship.

Eligible organisations that filed Form No. 10AB between 1 October 2025 and 31 March 2026 should ensure that they comply with all other requirements and follow up with the jurisdictional authorities for timely disposal of their applications.

Key Takeaways

- CBDT has condoned delay in filing Form No. 10AB.

- Relief is available for electronic applications filed between 1 October 2025 and 31 March 2026.

- Applies to renewal of approval under Section 80G(5).

- Previously rejected applications due only to delay will also be reconsidered.

- Applications must be decided on merits by 31 December 2026.

- The circular does not grant automatic approval; statutory conditions must still be satisfied.

Click here for PDF of the said Circular