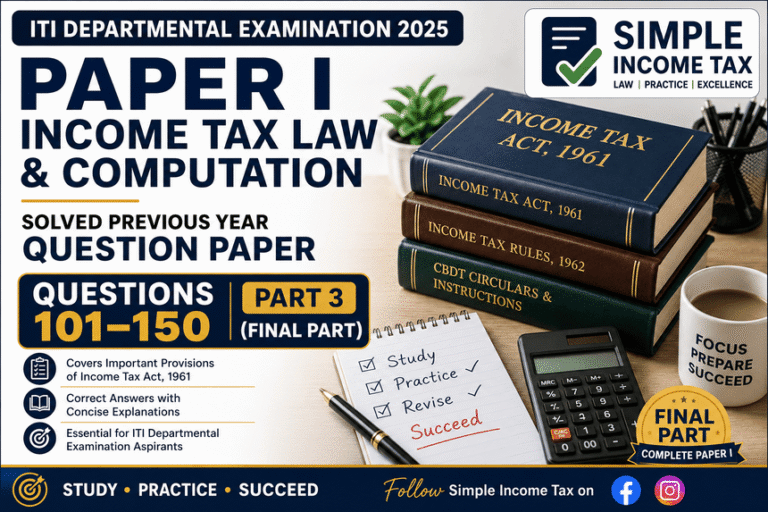

Preparing for the Income Tax Inspector (ITI) Departmental Examination means ITI Departmental Examination 2025 requires more than simply memorising the provisions of the Income Tax Act, 1961. Candidates are expected to possess a sound understanding of statutory provisions, departmental procedures, assessment practices, powers of Income Tax authorities, and the practical application of the law in day-to-day tax administration. Solving previous years’ question papers remains one of the most effective ways to assess preparation levels and identify important areas of the syllabus.

With the publication of Part 3, we complete the final segment of the Income Tax Inspector (ITI) Departmental Examination 2025 – Paper I (Income Tax Law & Computation) solved question paper series. This article contains Questions 101 to 150, along with the correct answers and concise explanations to facilitate quick revision before the departmental examination.

The questions included in this part primarily test the candidate’s understanding of assessment and reassessment proceedings, appeals and revisions, powers of Income Tax authorities, search and seizure, survey, penalties, prosecution, TDS and TCS provisions, recovery of tax, faceless proceedings, taxpayer services, digital compliance, and various procedural aspects of the Income Tax Act, 1961. These topics are of immense practical importance for officials working in the Income Tax Department and are consistently tested in departmental examinations.

As with the earlier parts of this series, every question has been reproduced from the original examination paper and is accompanied by:

- The correct answer.

- A brief explanation highlighting the relevant legal provision or principle.

- Reference to the applicable provisions of the Income Tax Act, wherever relevant.

The explanations have been intentionally kept concise to make this article an effective last-minute revision resource. Candidates are nevertheless encouraged to refer to the Income Tax Act, 1961, the Income Tax Rules, 1962, CBDT Notifications, Circulars, and departmental instructions for a more comprehensive understanding of the subject.

What This Part Covers

This article contains:

- Questions 101–150 of the original ITI Departmental Examination 2025.

- Correct answers with concise explanations.

- Questions based on practical departmental procedures and statutory provisions.

- Important topics frequently asked in Income Tax Departmental Examinations.

- A quick revision guide for Income Tax Inspector (ITI) aspirants.

Upon completion of this article, readers will have covered the entire Paper I (Questions 1–150) of the ITI Departmental Examination 2025, making this series a comprehensive reference for departmental examination preparation.

Previous Parts of This Series

- Part 1: Questions 1–50 – Fundamental provisions of the Income Tax Act, residential status, exemptions, capital gains, house property, business income, depreciation, charitable trusts, and unexplained income.

- Part 2: Questions 51–100 – Chapter VI-A deductions, carry forward and set-off of losses, corporate taxation, international taxation, search and seizure, jurisdiction, return filing, assessment procedures, and rectification.

Let’s now proceed with the final 50 questions (Questions 101–150) of Paper I – Income Tax Law & Computation and complete the solved previous year question paper series.

Q.101 Match the following:

(i) Section 143(1)

(ii) Section 143(3)

(iii) Section 144A

(iv) Section 144C

(a) (i)-a, (ii)-b, (iii)-c, (iv)-d

(b) (i)-b, (ii)-a, (iii)-d, (iv)-c

(c) (i)-b, (ii)-a, (iii)-c, (iv)-d

(d) (i)-a, (ii)-b, (iii)-d, (iv)-c

Correct Answer: (d)

Explanation: Section 143(1)-CPC Processing, 143(3)-Scrutiny Assessment, 144A-JCIT Directions, 144C-DRP.

Q.102 Where a firm does not comply with Section 184, the income of the firm shall be assessed:

(a) On estimation

(b) No deduction of interest, salary, bonus, commission or remuneration to partners shall be allowed.

(c) Such interest, salary, bonus, commission or remuneration shall not be taxable u/s 28(v).

(d) Both (b) and (c)

Correct Answer: (d)

Explanation: Non-compliance with Section 184 results in denial of partner remuneration deduction and corresponding non-taxability under Section 28(v).

Q.103 As per Section 151 (Finance Act, 2024), where three years or less have elapsed from the end of the relevant assessment year, approval for issuing notice under Sections 148A/148 shall be obtained from:

(a) PCCIT/PDGIT/CCIT/DGIT

(b) Additional Commissioner/Joint Commissioner

(c) PCIT/PDIT/CIT/DIT

(d) No approval required

Correct Answer: (b)

Explanation: Finance Act, 2024 substituted the specified authority with Additional Commissioner or Joint Commissioner.

Q.104 With effect from 01.09.2024, where escaped income is below Rs.50 lakh, the last date for issuing notice under Section 148A for AY 2022-23 is:

(a) 31.03.2025

(b) 31.03.2026

(c) 31.03.2027

(d) 31.03.2028

Correct Answer: (b)

Explanation: The amended limitation permits action up to 31.03.2026 in such cases.

Q.105 A revised return under Section 139(5) may be furnished:

(a) Before three months prior to the end of the relevant assessment year or completion of assessment, whichever is earlier.

(b) Before six months prior to the end of the relevant assessment year or completion of assessment.

(c) Before the end of the relevant assessment year or completion of assessment.

(d) Before one year from the end of the relevant assessment year or completion of assessment.

Correct Answer: (a)

Explanation: A revised return can be filed up to three months before the end of the assessment year or completion of assessment, whichever is earlier.

Q.106 From 01.09.2024, search assessments initiated under Section 132 are governed by:

(a) Section 158BA

(b) Section 147

(c) Section 156A

(d) Section 153A

Correct Answer: (a)

Explanation: Finance Act, 2024 introduced the new Block Assessment scheme under Chapter XIV-B.

Q.107 To carry forward losses, the return of loss must be furnished:

(a) On or before the due date under Section 139(1)

(b) Before the end of the assessment year

(c) Within one year from the end of the assessment year

(d) Before 31st October of the assessment year

Correct Answer: (a)

Explanation: Timely filing under Section 139(1) is mandatory for most loss carry forward claims.

Q.108 Under Section 163, an “agent” of a non-resident includes:

(a) Family member

(b) Employee or representative

(c) Person having business connection

(d) Both (b) and (c)

Correct Answer: (d)

Explanation: Section 163 includes representatives and persons having business connection with the non-resident.

Q.109 Under Section 194-I, “Rent” includes:

- Payment for use of land

- Payment for use of furniture under sub-lease

- Lease rent for land and machinery

- Sub-lease of land appurtenant to building

(a) 1,3,4

(b) 1,2,3

(c) 1,2,4

(d) 1,2,3,4

Correct Answer: (d)

Explanation: Section 194-I gives a very wide definition of rent covering all such payments.

Q.110 Regarding Section 194N, which statements are correct?

- Applicable to banks, cooperative banks and post offices.

- Applicable where each cash payment exceeds Rs.1 crore.

- Applicable where cumulative withdrawals exceed Rs.1 crore.

- For non-filers, applicable from cumulative withdrawals exceeding Rs.50 lakh.

(a) 1,3,4

(b) 1,2,4

(c) 1,2

(d) 1,3

Correct Answer: (a)

Explanation: The threshold is cumulative and lower for specified non-filers.

Q.111 Which statement regarding the Tax Recovery Officer is correct?

(a) Can attach only sale proceeds of immovable property.

(b) Can attach spouse’s bank account.

(c) Cannot attach property already attached by AO.

(d) Can manage commercial property and utilise rent towards tax recovery.

Correct Answer: (d)

Explanation: The TRO may appoint a receiver and utilise rental income for recovery.

Q.112 Which are obligations of a deductor under TDS provisions?

(i) Obtain PAN and deduct correct TDS.

(ii) Deposit TDS within due date.

(iii) Ensure deductee files ITR.

(iv) Verify authenticity of deductions claimed by deductee.

(a) Only (i) and (ii)

(b) Only (iii) and (iv)

(c) All

(d) None

Correct Answer: (a)

Explanation: Deductor’s statutory obligations end with proper deduction and deposit of TDS.

Q.113 Which statements regarding Advance Tax are correct?

(i) Section 87A rebate is considered.

(ii) TDS is considered.

(iii) Advance tax applies where tax liability is Rs.10,000 or more.

(iv) AO may issue demand under Section 156 for advance tax.

(a) (i),(ii),(iv)

(b) (i),(ii),(iii)

(c) All

(d) (ii),(iii),(iv)

Correct Answer: (b)

Explanation: The Assessing Officer cannot raise advance tax demand under Section 156.

Q.114 Which does NOT constitute “work” under Section 194C?

(a) Carriage of goods

(b) Consultancy services

(c) Catering

(d) Broadcasting

Correct Answer: (b)

Explanation: Professional consultancy services fall outside the scope of Section 194C.

Q.115 Section 195 primarily requires:

(a) No tax deduction

(b) Deduction of tax at source at prescribed rates

(c) Withholding entire payment

(d) Clearance certificate

Correct Answer: (b)

Explanation: Tax must be deducted from payments chargeable to tax made to non-residents.

Q.116 Section 197 provides for:

(a) TDS exemption

(b) Certificate for lower or nil deduction of tax

(c) Automatic refunds

(d) Revision of tax rates

Correct Answer: (b)

Explanation: Section 197 authorises issue of certificates for lower or nil TDS.

Q.117 Section 199 primarily deals with:

(a) Salary TDS

(b) Credit of TDS

(c) Non-resident tax slabs

(d) Profit computation

Correct Answer: (b)

Explanation: Section 199 governs the grant of TDS credit.

Q.118 Section 200 deals with:

(a) Computation of income

(b) Payment of tax deducted at source

(c) TDS exemption

(d) Filing return

Correct Answer: (b)

Explanation: Deducted tax must be deposited in accordance with Section 200.

Q.119 Failure to deposit tax deducted under Section 195 attracts consequences under:

(a) Section 201

(b) Section 202

(c) Section 203

(d) Section 204

Correct Answer: (a)

Explanation: Section 201 treats the deductor as an assessee in default.

Q.120 The main objective of Section 206C is:

(a) Eliminate TDS

(b) Collect tax at source on specified goods

(c) Automatic refunds

(d) Increase tax rates

Correct Answer: (b)

Explanation: TCS ensures tax collection at the point of specified transactions.

Question 121. Section 218 of the Income Tax Act provides guidelines for:

a) Calculation of interest on advance tax | b) Application for refund of TDS | c) Credit for tax deducted at source | d) Assessee deemed to be in default

Correct Answer: (d) Assessee deemed to be in default

Explanation: Section 218 treats a person as an assessee in default for failure to pay advance tax.

Question 122. Under Section 209, which of the following is NOT considered while computing advance tax liability?

a) Tax deducted at source (TDS) | b) Self-assessment tax paid under Section 140A | c) Tax collected at source (TCS) | d) Tax refunds from previous years

Correct Answer: (b) Self-assessment tax paid under Section 140A

Explanation: Self-assessment tax is paid after the financial year and is not considered while estimating advance tax.

Question 123. Which section governs TDS on income in respect of investment in a securitisation trust?

a) Section 194LBC | b) Section 194LBB | c) Section 194LC | d) Section 194LD

Correct Answer: (a) Section 194LBC

Explanation: Section 194LBC deals with TDS on income distributed by a securitisation trust.

Question 124. TDS deducted under Sections 194-IA and 194-IB shall be paid to the credit of the Central Government:

a) On or before 7th of the following month | b) On or before 15th of the following month | c) Within 30 days from the end of the month in which deduction is made | d) On or before 30th April of the next financial year

Correct Answer: (c) Within 30 days from the end of the month in which deduction is made

Explanation: Tax deducted under Sections 194-IA and 194-IB is deposited through Form 26QB/26QC within 30 days.

Question 125. CBDT Instruction No. 1914 relates to:

a) Capital gains on sale of shares | b) Carry forward of losses | c) Collection and recovery of tax arrears | d) Clubbing of income

Correct Answer: (c) Collection and recovery of tax arrears

Explanation: CBDT Instruction No. 1914 lays down guidelines for recovery and stay of demand.

Question 126. An application for revision under Section 264 by the assessee must be made within:

a) Six months | b) Two years | c) One year | d) Nine months

Correct Answer: (a) Six months

Explanation: An application under Section 264 must ordinarily be filed within six months from communication of the order or knowledge thereof.

Question 127. As per Section 271F, failure to furnish return of income before the end of the relevant assessment year attracts a penalty of:

a) Rs. 50,000 | b) Rs. 10,000 | c) Rs. 5,000 | d) Rs. 25,000

Correct Answer: (c) Rs. 5,000

Explanation: Section 271F (as applicable) prescribed a penalty of Rs. 5,000 for failure to furnish the return within the prescribed time.

Question 128. As per Section 260A, which of the following statements is incorrect?

a) High Court has no power to formulate substantial question of law itself. | b) Appeal shall be heard only on the substantial question of law formulated. | c) Appeal lies against every ITAT order involving substantial question of law. | d) Appeal is to be filed within 120 days.

Correct Answer: (a)

Explanation: The High Court itself formulates the substantial question of law before hearing the appeal.

Question 129. Under Section 282, service of notice may be effected through:

- Post/Courier approved by CBDT.

- Mode prescribed under the Code of Civil Procedure.

- Electronic mode notified by CBDT.

a) Option (1) | b) Option (2) | c) Option (3) | d) None of the above

Correct Answer: (d) None of the above

Explanation: Section 282 recognises all the prescribed modes of service.

Question 130. Which section deals with the obligation to furnish Statement of Financial Transactions (SFT)?

a) Section 285BBA | b) Section 285BA | c) Section 285BB | d) None

Correct Answer: (b) Section 285BA

Explanation: Section 285BA mandates furnishing of Statement of Financial Transactions.

Question 131. Penalty for contravention of Section 269SS is imposed under:

a) Section 271C | b) Section 271D | c) Section 271E | d) Section 271F

Correct Answer: (b) Section 271D

Explanation: Section 271D imposes penalty equal to the amount of loan or deposit accepted in contravention of Section 269SS.

Question 132. Which of the following statements is incorrect?

a) Revision under Section 263 can be made within two years. | b) Revision under Section 264 has a one-year limitation in specified cases. | c) Revision under Section 263 can be done only on the application of the Assessing Officer. | d) Revision under Section 264 can be initiated suo motu.

Correct Answer: (c)

Explanation: The Principal Commissioner may invoke Section 263 suo motu and not merely on an AO’s application.

Question 133. Section 281 regarding certain transfers being void does NOT apply to:

a) Land | b) Fixed Deposits | c) Stock-in-trade | d) Plant & Machinery

Correct Answer: (c) Stock-in-trade

Explanation: Transfers made in the ordinary course of business, including stock-in-trade, are outside the scope of Section 281.

Question 134. A dissolved firm is to be served with a notice. Which of the following is NOT a valid service?

a) Service on the managing partner before dissolution. | b) Service on a minor partner. | c) Service on one of the original partners. | d) None of the above.

Correct Answer: (b) Service on a minor partner

Explanation: A minor partner is not competent to receive statutory notice on behalf of the firm.

Question 135. Penalty under Section 270A for claim of expenditure not substantiated by evidence is:

a) 50% of tax payable on under-reported income | b) 50% of tax sought to be evaded | c) 200% of tax payable on under-reported income | d) 200% of tax sought to be evaded

Correct Answer: (c)

Explanation: Misreporting of income attracts a penalty of 200% of the tax payable on under-reported income.

Question 136. Penalty relating to addition under Section 68 for AY 2024-25 is leviable under:

a) Section 270A | b) Section 271AAB | c) Section 271AAC | d) Section 271AAD

Correct Answer: (c) Section 271AAC

Explanation: Section 271AAC prescribes penalty for income determined under Sections 68 to 69D.

Question 137. Match the following:

- Section 269SS

- Section 269ST

- Section 269T

- Section 269SU

a) 1-i, 2-ii, 3-iii, 4-iv | b) 1-ii, 2-iv, 3-iii, 4-i | c) 1-iv, 2-i, 3-ii, 4-iii | d) 1-iv, 2-iii, 3-i, 4-ii

Correct Answer: (c)

Explanation: Sections 271D, 271DA, 271E and 271DB correspond to Sections 269SS, 269ST, 269T and 269SU respectively.

Question 138. Penalty under Section 271G for failure to furnish information/documents under Section 92D is:

a) Rs. 10,000 per transaction | b) Rs. 25,000 per transaction | c) 1% of transaction value | d) 2% of transaction value

Correct Answer: (d) 2% of transaction value

Explanation: Section 271G provides for penalty at 2% of the value of each international or specified domestic transaction.

Question 139. Mr. X repays a loan of Rs. 2,00,000 in cash to Mr. Y. Which statement is correct?

a) Only (i) | b) Only (iii) | c) Only (ii) | d) None

Correct Answer: (b) Only (iii)

Explanation: Repayment of loan in cash violates Section 269T, attracting penalty under Section 271E on the person making the repayment.

Question 140. Penalty for failure to answer questions, sign statements, furnish information, allow inspection, etc., is leviable under:

a) Section 272 | b) Section 272A | c) Section 272AA | d) Section 272B

Correct Answer: (b) Section 272A

Explanation: Section 272A provides for penalties for failure to comply with various statutory obligations under the Income Tax Act.

Question 141. The time limit for passing an order of assessment or reassessment under Section 10 of the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 is:

a) Two years from the end of the month in which notice under Section 10(1) is issued. | b) Three years from the end of the financial year. | c) Two years from the end of the financial year. | d) None of the above.

Correct Answer: (a) Two years from the end of the month in which notice under Section 10(1) is issued.

Explanation: Section 10 of the Black Money Act prescribes a two-year limitation from the end of the month of issuance of notice.

Question 142. What is the definition of an undisclosed asset located outside India under the Black Money Act, 2015?

a) An asset located outside India held in the assessee’s name without satisfactory explanation of the source of investment. | b) Financial interest in an entity located outside India without satisfactory explanation of the source. | c) Asset located outside India in respect of which the Assessing Officer is not satisfied with the explanation regarding the source of investment. | d) All of the above.

Correct Answer: (d) All of the above

Explanation: The definition covers undisclosed foreign assets and financial interests where the source of investment remains unexplained.

Question 143. Match the following provisions of the Black Money Act:

- Section 10

- Section 11

- Section 12

- Section 13

a) 1-A, 2-B, 3-C, 4-D | b) 1-D, 2-C, 3-B, 4-A | c) 1-C, 2-A, 3-D, 4-B | d) 1-B, 2-D, 3-A, 4-C

Correct Answer: (b) 1-D, 2-C, 3-B, 4-A

Explanation: Sections 10, 11, 12 and 13 respectively deal with assessment, time limit, rectification of mistakes and notice of demand.

Question 144. Consider the following statements regarding the Black Money Act, 2015:

(i) Assessment or reassessment under Section 10 cannot be made after two years from the end of the month in which notice under Section 10(1) is issued.

(ii) A fresh assessment pursuant to an order under Section 18 may be made within two years from the end of the financial year in which such order is received by the Principal Commissioner or Commissioner.

a) Both (i) and (ii) are correct. | b) Both (i) and (ii) are incorrect. | c) Only (i) is correct. | d) Only (ii) is correct.

Correct Answer: (a) Both (i) and (ii) are correct

Explanation: Both statements correctly reproduce the limitation provisions under the Black Money Act.

Question 145. The Prohibition of Benami Property Transactions Act, 1988 was enacted on the recommendations of:

a) 57th Law Commission | b) Tax Administrative Reforms Commission | c) 130th Law Commission | d) Second Administrative Reforms Commission

Correct Answer: (a) 57th Law Commission

Explanation: The Benami law was enacted pursuant to the recommendations of the 57th Report of the Law Commission of India.

Question 146. Which of the following correctly describes a ‘Benami Transaction’ under the Prohibition of Benami Property Transactions Act, 1988?

a) Property is transferred to or held by one person while consideration is paid by another person. | b) The property is held for the direct or indirect benefit of the person providing the consideration. | c) Both (a) and (b). | d) None of the above.

Correct Answer: (c) Both (a) and (b)

Explanation: A benami transaction involves property held by one person for the benefit of another who has provided the consideration.

Question 147. Which of the following authorities is NOT established under the Prohibition of Benami Property Transactions Act, 1988?

a) Initiating Officer | b) Approving Authority | c) Prosecuting Authority | d) Adjudicating Authority

Correct Answer: (c) Prosecuting Authority

Explanation: The PBPT Act provides for Initiating Officer, Approving Authority and Adjudicating Authority, but not a separate Prosecuting Authority.

Question 148. Proceedings under the Prohibition of Benami Property Transactions Act, 1988 commence with the issue of a Show Cause Notice under:

a) Section 24(1) | b) Section 24(3) | c) Section 24(4) | d) Section 19(1)

Correct Answer: (a) Section 24(1)

Explanation: Proceedings begin with the issue of a Show Cause Notice by the Initiating Officer under Section 24(1).

Question 149. Who is the competent authority to sanction prosecution in Benami cases?

a) DGIT (Investigation) | b) Principal Director of Income Tax (Investigation) | c) Approving Authority | d) Principal Chief Commissioner of Income Tax (CCA)

Correct Answer: (d) Principal Chief Commissioner of Income Tax (CCA)

Explanation: Sanction for prosecution under the PBPT Act is accorded by the Principal Chief Commissioner of Income Tax (CCA).

Question 150. If a property is declared benami, can the beneficial owner legally claim the property under any circumstances?

a) Yes, by proving genuine ownership. | b) Yes, by filing a civil suit. | c) No, the property is liable to confiscation without payment of compensation. | d) Yes, after payment of penalty.

Correct Answer: (c) No, the property is liable to confiscation without payment of compensation.

Explanation: Under the PBPT Act, benami property stands confiscated by the Central Government without payment of compensation to the beneficial owner.

Conclusion

With this article, we have successfully completed the entire Paper I of the Income Tax Inspector (ITI) Departmental Examination 2025, thereby concluding our comprehensive three-part series covering all 150 objective questions with correct answers and concise explanations.

The final section of the paper focuses extensively on assessment and reassessment proceedings, TDS and TCS provisions, recovery of tax, revision, appeals, penalties, prosecution, the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015, the Prohibition of Benami Property Transactions Act, 1988, and other important procedural provisions. These subjects are not only relevant for the departmental examination but also form an integral part of the day-to-day responsibilities of officers of the Income Tax Department. A thorough understanding of these provisions will significantly enhance both examination performance and practical application in official work.

A review of the complete Paper I reveals that the Departmental Examination is increasingly concept-oriented, with considerable emphasis on recent legislative amendments, practical scenarios, procedural provisions, and departmental instructions. Candidates should therefore supplement their preparation with regular study of the Income Tax Act, 1961, the Income Tax Rules, 1962, relevant Finance Acts, CBDT Circulars, Notifications, Instructions, and important judicial pronouncements instead of relying solely on memorisation of section numbers.

This three-part solved question paper series is intended to serve as a reliable revision guide for officials preparing for the Income Tax Inspector Departmental Examination. However, aspirants are encouraged to first attempt each question independently and then compare their answers with the explanations provided. This approach strengthens conceptual clarity, improves retention, and develops the analytical skills required for objective-type departmental examinations.

We hope this series proves to be a valuable resource for every officer aspiring to succeed in the Income Tax Inspector Departmental Examination. If you found these articles useful, consider bookmarking this series, sharing it with your colleagues, and following Simple Income Tax for regular updates, study material, departmental examination resources, and the latest developments in Income Tax law and administration.

Completed Series

✅ Part 1: Questions 1–50 – Solved with Answers & Explanations

✅ Part 2: Questions 51–100 – Solved with Answers & Explanations

✅ Part 3: Questions 101–150 – Solved with Answers & Explanations

Thank you for reading. Best wishes for your preparation and success in the Income Tax Inspector Departmental Examination!

Always refer to Official Income Income Tax Act