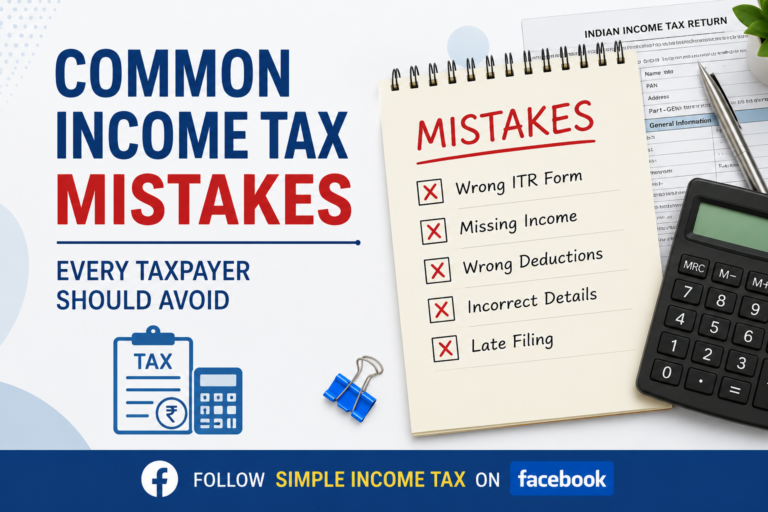

Filing an Income Tax Return (ITR) has become much easier with the availability of online filing, pre-filled information and digital verification. However, many taxpayers still make small mistakes that can result in delayed refunds, notices from the Income Tax Department, additional tax liability, penalties or prolonged litigation. In most cases, these mistakes are unintentional and can easily be avoided with proper care while filing the return.

Whether you are a salaried employee, pensioner, professional, freelancer, business owner or senior citizen, understanding these common errors can help you file an accurate return and avoid future problems. In this article, we discuss the most common Income Tax mistakes and practical ways to avoid them.

Why Accuracy in Income Tax Return Filing Matters

An Income Tax Return is more than just a formality. It is a legal declaration of your income, deductions, exemptions, taxes paid and other financial information. The Income Tax Department now uses Artificial Intelligence (AI), Annual Information Statement (AIS), Taxpayer Information Summary (TIS), Form 26AS, Statement of Financial Transactions (SFT) and various third-party databases to verify information submitted by taxpayers.

Even a small mismatch between your return and the information available with the department can trigger notices or scrutiny. Therefore, taxpayers should verify every detail carefully before submitting the return.

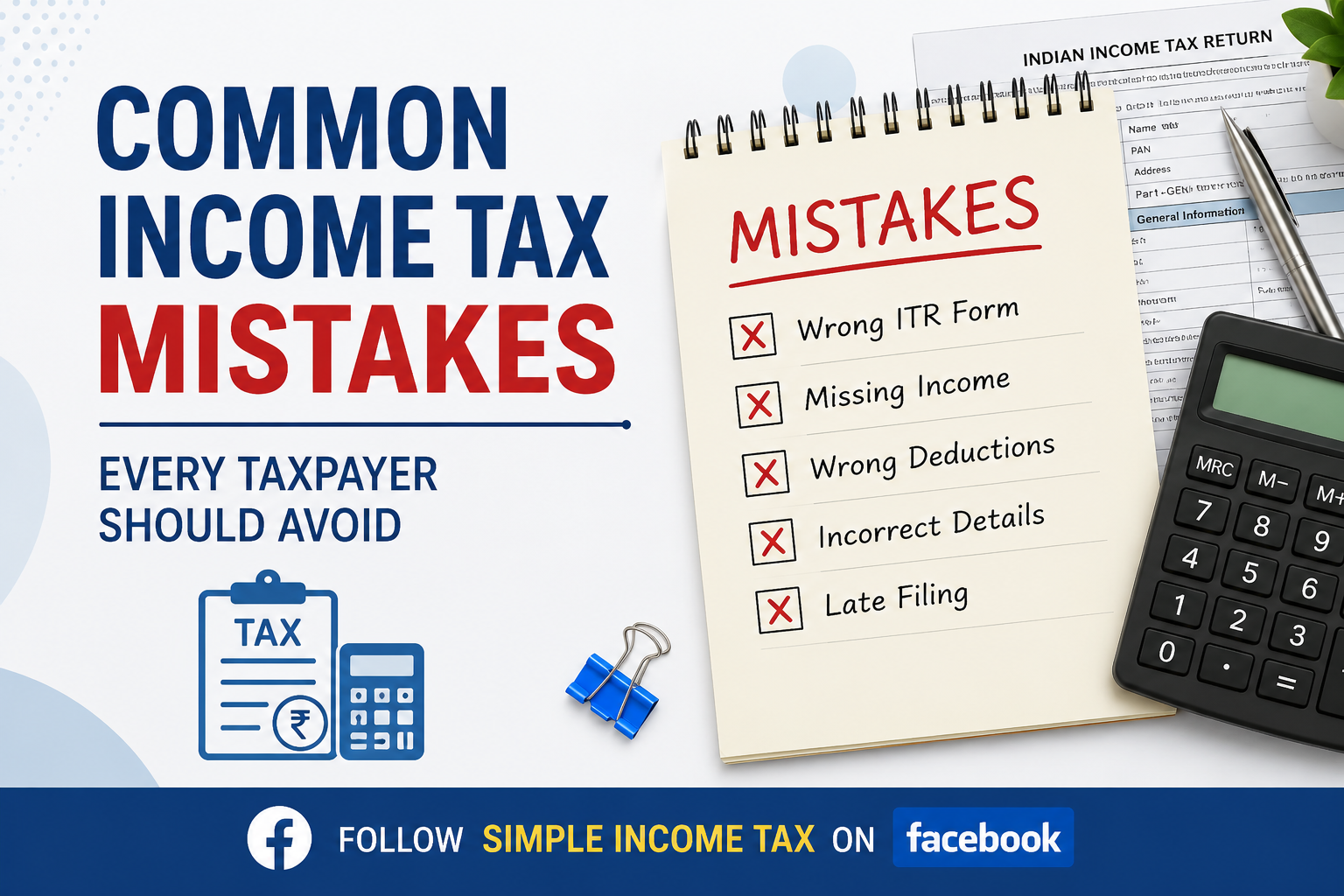

1. Choosing the Wrong ITR Form

One of the most common mistakes is selecting the wrong Income Tax Return form.

Every ITR form is designed for a specific category of taxpayers. Filing an incorrect form may lead to the return being treated as defective, requiring correction or fresh filing.

Before filing your return, always check whether you should file ITR-1, ITR-2, ITR-3, ITR-4 or any other applicable form based on your sources of income.

2. Not Verifying AIS and Form 26AS

Many taxpayers file returns solely on the basis of Form 16 or their own records.

However, the Income Tax Department compares your return with information available in:

- Annual Information Statement (AIS)

- Taxpayer Information Summary (TIS)

- Form 26AS

If any income reflected in these records is omitted from your return, it may result in a notice.

Always compare your return with AIS and Form 26AS before filing.

3. Forgetting Interest Income

Interest earned from savings accounts, fixed deposits, recurring deposits and post office deposits is frequently omitted while filing returns.

Banks report such interest to the Income Tax Department.

Even if TDS has not been deducted, interest income may still be taxable and should be reported appropriately.

4. Claiming Wrong Deductions

Many taxpayers claim deductions without checking whether they satisfy the conditions prescribed under the Income Tax Act.

Examples include:

- Section 80C

- Section 80D

- Section 80E

- Section 80G

- Section 80CCD

Claiming deductions without supporting documents or eligibility may result in disallowance, additional tax demand, interest, and in certain cases, penalty.

5. Forgetting Additional Income

Many individuals have multiple sources of income such as:

- Rental income

- Freelance income

- Dividend income

- Capital gains

- Family pension

- Interest income

- Foreign income

Every taxable income should be reported correctly.

6. Wrong Bank Account Details

Refunds are directly credited into the bank account mentioned in the return.

Entering an incorrect account number or IFSC code may delay refunds significantly.

Always verify your bank details before filing.

7. Not Reporting Capital Gains

Many taxpayers believe that only salary is taxable.

However, gains from selling:

- Shares

- Mutual Funds

- Property

- Gold

- Bonds

- Cryptocurrency (where applicable)

may also be taxable.

Failure to report capital gains is one of the major reasons for departmental notices.

8. Ignoring Foreign Assets

Resident taxpayers are required to disclose foreign assets and foreign income wherever applicable.

The Income Tax Department receives information through international information-sharing agreements.

Non-disclosure may attract severe consequences.

9. Claiming Exemptions Without Eligibility

Many salaried employees claim exemptions for:

- House Rent Allowance (HRA)

- Leave Travel Allowance (LTA)

- Other reimbursements

without satisfying the prescribed conditions.

Always ensure that exemption claims are supported by proper documents.

10. Not Reporting High-Value Financial Transactions

Large financial transactions are reported to the Income Tax Department through the Statement of Financial Transactions (SFT).

These include:

- Large cash deposits

- High-value property purchases

- Mutual fund investments

- Credit card payments

- Fixed deposits

If these transactions are not properly explained through your return, they may attract verification.

11. Missing the ITR Filing Due Date

Late filing may result in:

- Late filing fee

- Interest

- Delay in refund

- Carry forward restrictions for certain losses

Always file your return before the due date.

12. Not Revising the Return After Discovering Mistakes

Many taxpayers discover mistakes after filing but assume nothing can be done.

The Income Tax Act permits filing of a revised return within the prescribed time limit.

If you identify any error, revise the return immediately instead of waiting for a departmental notice.

13. Ignoring Income Tax Notices

Ignoring notices is one of the biggest mistakes.

Many notices seek only clarification or additional information.

Responding within the prescribed time often resolves the matter quickly.

Ignoring notices may lead to further proceedings.

14. Not Keeping Supporting Documents

Although documents generally need not be attached with the return, taxpayers should preserve:

- Form 16

- Investment proofs

- Medical insurance receipts

- Donation receipts

- Home loan certificates

- Capital gain calculations

- Bank statements

These documents may be required during verification or assessment.

15. Depending Entirely on Others

Many taxpayers file returns through friends, agents or tax preparers without reviewing the final return.

Since the taxpayer is legally responsible for the contents of the return, always review every figure before submission.

How to Avoid These Mistakes

The easiest way to avoid errors is to review your return carefully before filing. Compare all income with Form 16, Form 26AS, AIS and TIS. Keep supporting documents ready, verify deduction claims, check bank details, report all sources of income, and complete e-verification immediately after filing.

If you are unsure about any provision, seek professional guidance instead of making assumptions.

Final Thoughts

Most Income Tax mistakes are avoidable. Spending a little extra time while preparing your Income Tax Return can save you from notices, penalties, interest, and unnecessary litigation. As the Income Tax Department increasingly relies on technology, data analytics and AI-based verification, accurate reporting has become more important than ever.

A carefully prepared Income Tax Return not only ensures smooth processing of refunds but also builds a strong compliance record for future financial transactions such as loans, visas, and investments.

Related Articles on Simple Income Tax

Section 148A Notice Guide: HRA, 80C, NPS & Tax Deductions

If unsupported deductions or exemptions are claimed while filing your Income Tax Return, the Income Tax Department may initiate verification proceedings. This detailed guide explains the documents taxpayers should maintain, common mistakes noticed during assessments, and how to respond to notices under Section 148A.

Read here:

https://simpleincometax.online/section-148a-notice-guide-hra-80c-nps-tax-deductions/

Ready to file your ITR?

You can file your Income Tax Return online using the official Income Tax Department e-Filing Portal. Before filing, make sure you have verified your PAN, Aadhaar, Form 26AS, AIS, TIS, and all supporting documents to ensure an accurate return.